For many months economists and market strategists have suggested that a pending Federal Reserve “pivot” from policy stasis to sustained rate cutting will boost equity prices or at least preclude them from declining. Lewis Krauskopf at Reuters last July wrote that “Rate Cut Prospects Could Bolster US Stocks as Investors Await Earnings, Elections.” That same month, more than a third of respondents to Bank of America’s monthly Global Fund Manager Survey agreed that “monetary policy is too restrictive, the most restrictive since November 2008,” yet they also revealed that their investment portfolios remained “overweight in equities and underweight in bonds” (“Investors Remain Bullish Driven by the Expected Fed Rate Cuts,” Funds Society, July 19, 2024). At Morningstar last month, Gordon Gottsegen reported that “Retail Investors are Bullish on Stocks Ahead of the Fed’s Rate Cut Next Month.”

In fact, decades of investment history surrounding Fed policy pivots from rate stasis to rate cutting show that cutting has rarely been bullish for equities if the cuts came in the wake of yield curve inversions (which reliably forecast recessions). This distinction is relevant today because there’s strong and growing evidence that the next US recession has begun already – or will begin soon – because the yield curve has been inverted since late 2022 and remains so.

Many economists and strategists remain unsure about a pending US recession, having not forecasted it in the first place, or because generally they doubt that something’s real until it already passes them by. Similarly tardy will be the National Bureau of Economic Research, but that’s by design, because it assigns “official” dates to the start and finish of each recession, so before it makes its public pronouncements it wants to be sure about the final status of oft-revised economic data. Unfortunately, such “back-casting” (and even the New York Fed’s “nowcasting”) doesn’t help those who need foresight and time to adjust ahead of the trouble.

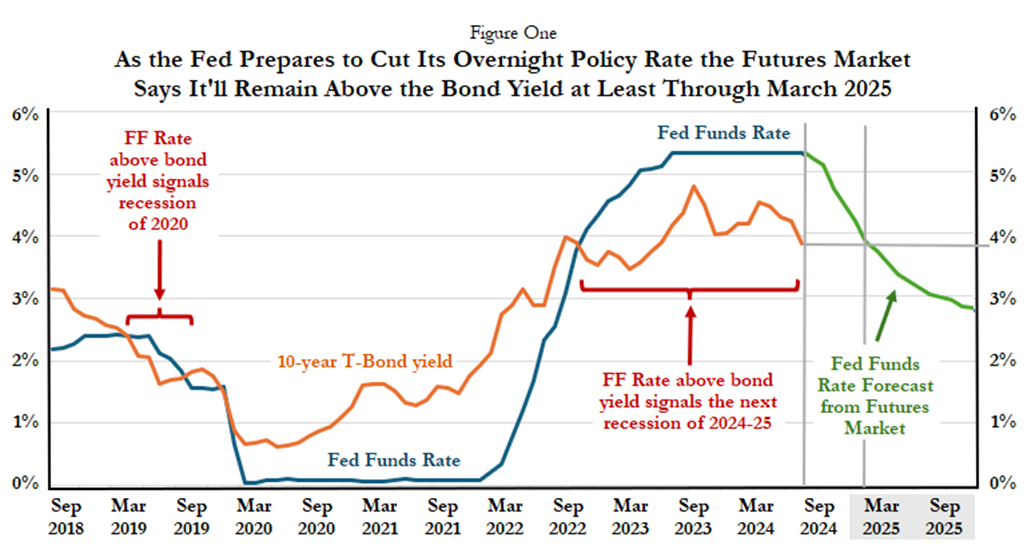

At the Fed’s Jackson Hole conference last month officials signaled a series of rate cuts to begin soon at FOMC meetings. It would be the first rate cutting since March 2020. Figure One plots the Fed funds rate versus the 10-year T-Bond yield over the past six years and includes a year-ahead forecast of the Fed rate derived from futures contracts. The projection is for cuts leading to a rate of 2.75 percent a year from now. Today’s rate is 5.25 percent, so moves to 2.75 percent would equal total cuts of 250 basis points. Bond yields typically decline amid rate cutting, so the yield curve might remain inverted at least through next March.

If this is the Fed’s coming move – cutting its policy rate substantially and quickly – it suggests a panicky policy; it betrays both a fearfulness and an eagerness to fight a recession which the Fed itself helped instigate by its previous, excessive, curve-inverting rate hikes.

Rate cutting typically recognizes the problem (recession) after the fact but doesn’t prevent the problem. Nor does rate cutting necessarily boost equities. It’s true that lower interest rates (long and short) tend to be bullish for equities “all else equal” (a lower discount factor applied to corporate earnings), but “all else” is not equal now; a recession means economic growth contracts and earnings decline, both of which undermine equity prices. Significant, rapid rate-cutting usually coincides not with an economic “soft landing” but incoming recession data. Rate cuts based on hindsight instead of foresight can confirm a recession but can’t prevent it.

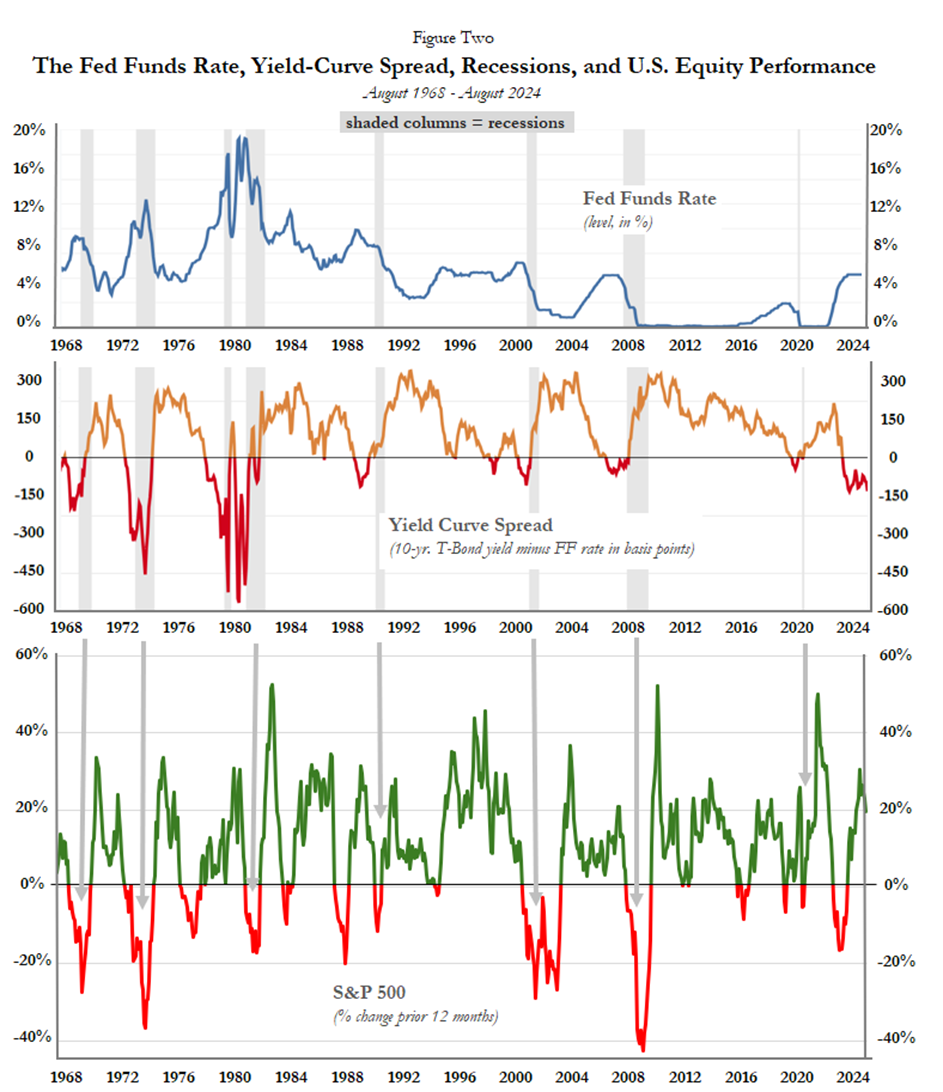

Important relationships among Fed policy, the yield curve spread, recessions, and equity performance since 1968 are illustrated in Figure Two. All eight recessions have been reliably preceded (roughly 12-18 months in advance) by Fed rate hiking that caused an inverted yield curve (depicted here as a negative yield curve spread, when short term interest rates lie above long-term bond yields). In all these years, we find no case of a recession occurring after no prior curve inversion and no case of a recession failing to occur despite a prior inversion.

I count eleven episodes of persistent and material Fed rate cutting since 1968 (Figure Two). Eight cases came on the heels of curve inversion and three occurred after no prior inversion. Only in the three other cases did Fed rate cutting not coincide with recession and plunging equity prices. The three cases are 1971-72, 1984-86, and 1995-98. They’re worth summarizing.

- Case #1 – In September 1971 the Fed began to cut its policy rate, then at 5.75 percent, to a low of 3.50 percent in January 1972. When the rate-cutting began, the yield curve was upward sloping (not inverted). The long-short rate spread was positive (62 basis points). There had been a prior recession (from December 1969 to November of 1970) but amid the rate cutting of 1971-72, economic growth persisted, and the S&P 500 gained 8 percent. The next recession would occur in 1973-75.

- Case #2 – In July 1984 the Fed initiated another benign episode of rate cutting. Over a two-year period, it reduced its policy rate dramatically, from 11.63 percent to 5.88 percent (by August 1986). When the cuts began, the yield curve again was upward sloping; the curve spread was positive (106 basis points). There was a prior recession (July 1981 to November 1982), but during this rate cutting period economic growth again held up, while the S&P 500 boomed by 44 percent. The next recession wouldn’t take hold until July 1990 (and last briefly, through March 1991).

- Case #3 – In April 1995 the Fed began to cut its then peak rate of 6.00 percent until by November 1998 it was down to 4.75 percent. The slow and steady policy was dubbed “gradualism.” Ten separate cuts totaled only 1.25 percentage points over three-and-a-half years. The yield curve was upward sloping when cutting began (a positive spread of 103 basis points). During this period the US economy was robust: real GDP growth was fast to begin with (+4.4 percent in 1996) and then accelerated to 4.5 percent in 1997 and 4.9 percent in 1998. During this episode the S&P 500 skyrocketed by 125 percent (37 percent annualized).

The impression held by today’s economists and strategists that Fed rate cutting is bullish for both output and equities might be skewed by these three cases – these few outliers. But digging more deeply and carefully into the data, we discover this fascinating phenomenon: that unlike the other eight cases, the three rate-cutting episodes of 1971-72, 1984-86, and 1995-98 (when the S&P 500 gained 8 percent, 44 percent, and 125 percent, respectively) were not preceded by a recession-signaling inverted yield curve.

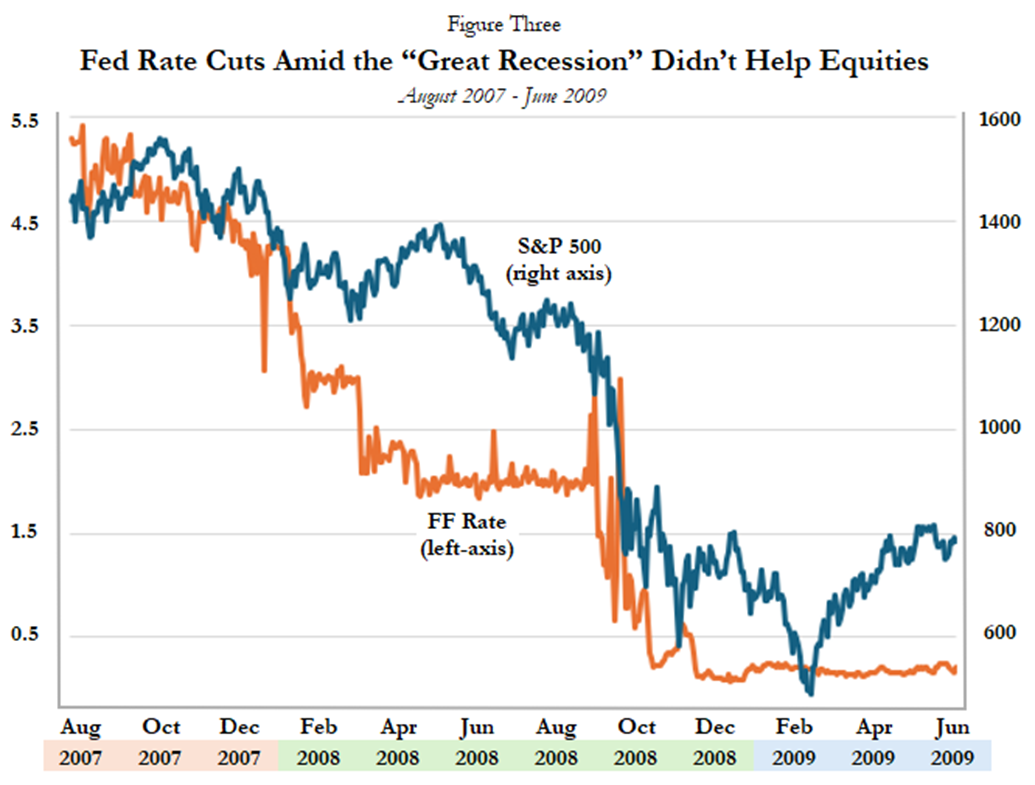

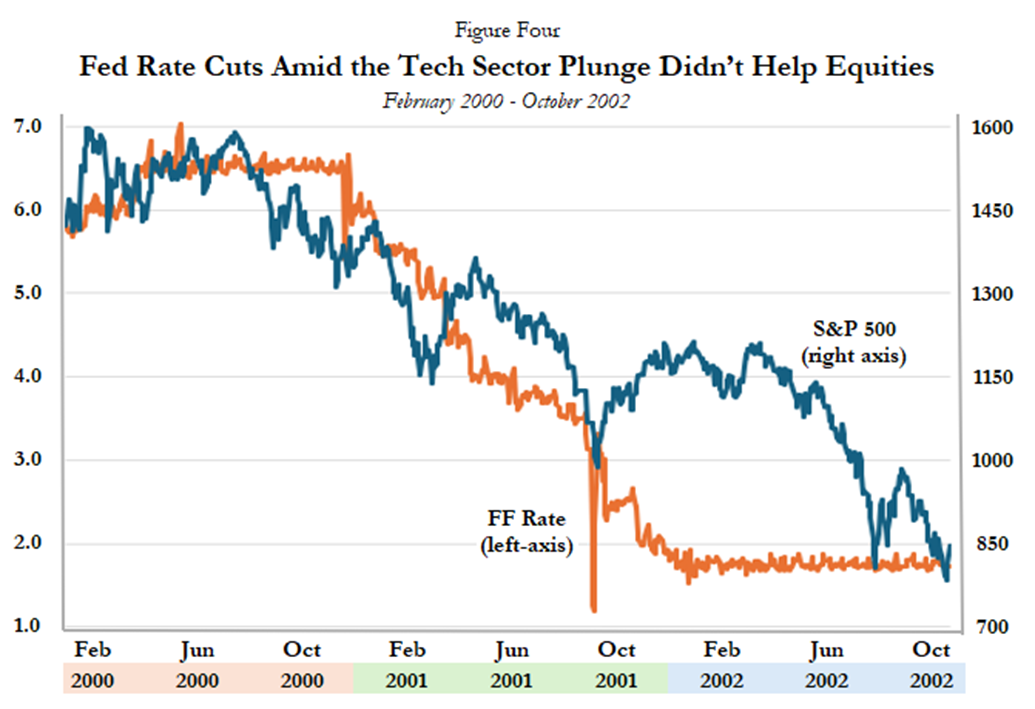

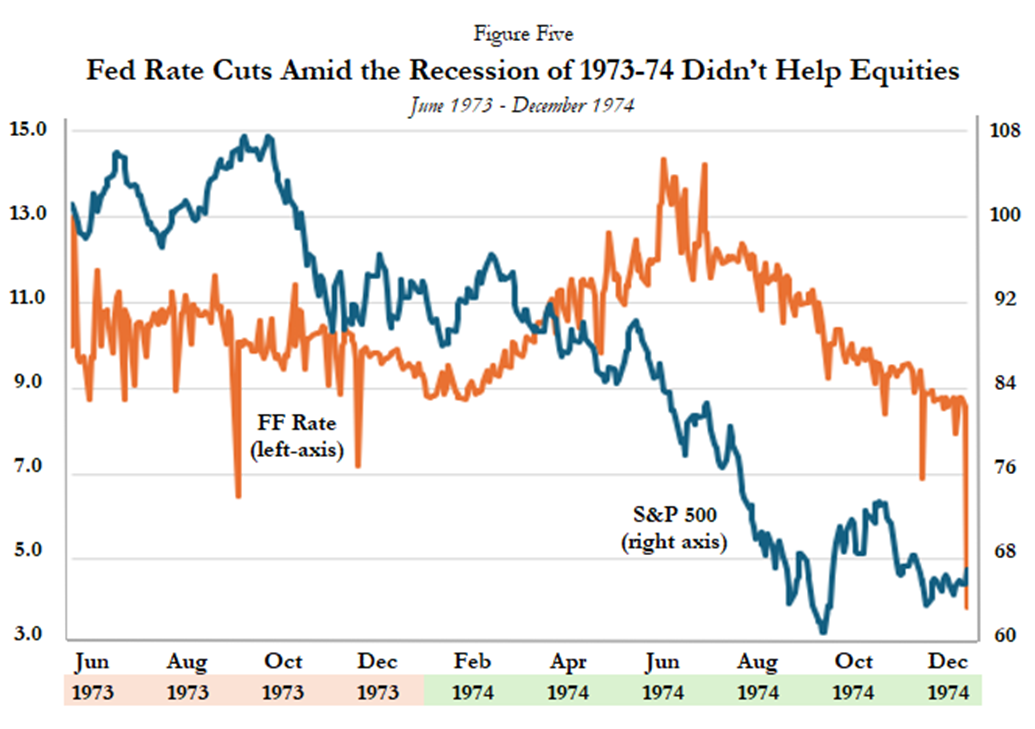

Now consider depictions (in Figures Three, Four and Five) of three major US recessions that occurred alongside severe Fed rate cutting. In these cases, US equity prices plunged “despite” Fed rate cutting. These are three of the eight typical cases of bearishness amid rate cutting witnessed since 1968 (when rate cutting arrived in the wake of an inverted yield curve). That’s precisely our current situation. It’s an ominous pattern — for those still bullish on equities.

For the entire period in Figure Three (August 2007 to June 2009), the S&P 500 declined by 36 percent (20 percent annualized), but the index was down by an astounding 51 percent from peak (October 2007) to trough (March 2009).

For the whole period in Figure Four the S&P 500 declined by 38 percent (25 percent annualized), but the index dropped 41 percent from peak (December 1999) to trough (February 2003).

In Figure Four, the S&P 500 declined by 36 percent (24 percent annualized), but the index fell farther (-44 percent) from peak (October 1973) to trough (October 1974).

Considering all relevant data and pertinent causal aspects surrounding Fed rate cutting in recent decades, it seems more likely than not that the next episode will neither prevent a US recession nor preclude a material decline in US equity prices. Of greatest relevance is the prior inversion of the yield curve and the more recent indication that recession may be here already or else imminent (due to the uptick in the jobless rate, per the “Sahm Rule Recession Indicator”). The fact that only three of the past eleven episodes of Fed cutting coincided with a growing US economy and rising US stock prices should be of little comfort today, when it’s realized that those cases weren’t preceded by an inverted yield curve or ominous Sahm signal.